As I know, there is no R(or Statsmodels)-like summary table in sklearn. (Please check this answer)

Instead, if you need it, there is statsmodels.regression.linear_model.OLS.fit_regularized class. (L1_wt=0 for ridge regression.)

For now, it seems that model.fit_regularized(~).summary() returns None despite of docstring below. But the object has params, summary() can be used somehow.

Returns: A RegressionResults object, of the same type returned by fit.

Example.

Sample data is not for ridge regression, but I will try anyway.

In.

import numpy as np

import pandas as pd

import statsmodels

import statsmodels.api as sm

import matplotlib.pyplot as plt

statsmodels.__version__

Out.

'0.8.0rc1'

In.

data = sm.datasets.ccard.load()

print "endog: " + data.endog_name

print "exog: " + ', '.join(data.exog_name)

data.exog[:5, :]

Out.

endog: AVGEXP

exog: AGE, INCOME, INCOMESQ, OWNRENT

Out[2]:

array([[ 38. , 4.52 , 20.4304, 1. ],

[ 33. , 2.42 , 5.8564, 0. ],

[ 34. , 4.5 , 20.25 , 1. ],

[ 31. , 2.54 , 6.4516, 0. ],

[ 32. , 9.79 , 95.8441, 1. ]])

In.

y, X = data.endog, data.exog

model = sm.OLS(y, X)

results_fu = model.fit()

print results_fu.summary()

Out.

OLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.543

Model: OLS Adj. R-squared: 0.516

Method: Least Squares F-statistic: 20.22

Date: Wed, 19 Oct 2016 Prob (F-statistic): 5.24e-11

Time: 17:22:48 Log-Likelihood: -507.24

No. Observations: 72 AIC: 1022.

Df Residuals: 68 BIC: 1032.

Df Model: 4

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

x1 -6.8112 4.551 -1.497 0.139 -15.892 2.270

x2 175.8245 63.743 2.758 0.007 48.628 303.021

x3 -9.7235 6.030 -1.613 0.111 -21.756 2.309

x4 54.7496 80.044 0.684 0.496 -104.977 214.476

==============================================================================

Omnibus: 76.325 Durbin-Watson: 1.692

Prob(Omnibus): 0.000 Jarque-Bera (JB): 649.447

Skew: 3.194 Prob(JB): 9.42e-142

Kurtosis: 16.255 Cond. No. 87.5

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

In.

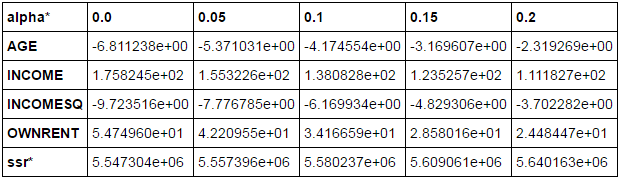

frames = []

for n in np.arange(0, 0.25, 0.05).tolist():

results_fr = model.fit_regularized(L1_wt=0, alpha=n, start_params=results_fu.params)

results_fr_fit = sm.regression.linear_model.OLSResults(model,

results_fr.params,

model.normalized_cov_params)

frames.append(np.append(results_fr.params, results_fr_fit.ssr))

df = pd.DataFrame(frames, columns=data.exog_name + ['ssr*'])

df.index=np.arange(0, 0.25, 0.05).tolist()

df.index.name = 'alpha*'

df.T

Out.

![enter image description here]()

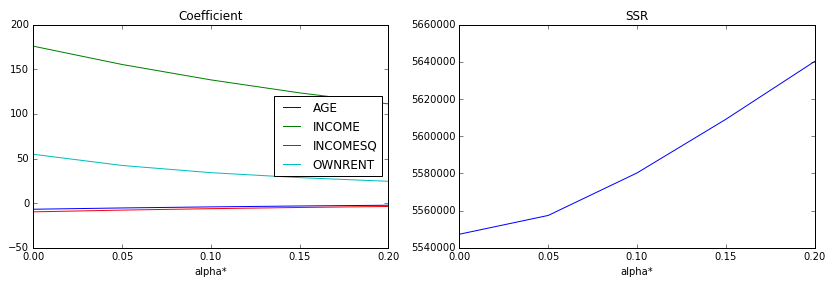

In.

%matplotlib inline

fig, ax = plt.subplots(1, 2, figsize=(14, 4))

ax[0] = df.iloc[:, :-1].plot(ax=ax[0])

ax[0].set_title('Coefficient')

ax[1] = df.iloc[:, -1].plot(ax=ax[1])

ax[1].set_title('SSR')

Out.

![enter image description here]()

In.

results_fr = model.fit_regularized(L1_wt=0, alpha=0.04, start_params=results_fu.params)

final = sm.regression.linear_model.OLSResults(model,

results_fr.params,

model.normalized_cov_params)

print final.summary()

Out.

OLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.543

Model: OLS Adj. R-squared: 0.516

Method: Least Squares F-statistic: 20.17

Date: Wed, 19 Oct 2016 Prob (F-statistic): 5.46e-11

Time: 17:22:49 Log-Likelihood: -507.28

No. Observations: 72 AIC: 1023.

Df Residuals: 68 BIC: 1032.

Df Model: 4

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

x1 -5.6375 4.554 -1.238 0.220 -14.724 3.449

x2 159.1412 63.781 2.495 0.015 31.867 286.415

x3 -8.1360 6.034 -1.348 0.182 -20.176 3.904

x4 44.2597 80.093 0.553 0.582 -115.564 204.083

==============================================================================

Omnibus: 76.819 Durbin-Watson: 1.694

Prob(Omnibus): 0.000 Jarque-Bera (JB): 658.948

Skew: 3.220 Prob(JB): 8.15e-144

Kurtosis: 16.348 Cond. No. 87.5

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.