I learned this technique from Jason Brownlee, PhD and author of more than 18 books having to do with Applied Machine Learning, Mathematics, and Statistics:

To give proper credit where is due, I am citing my source of the learning I achieved through this material:

Citing reference Book:

Introduction to Time Series Forecasting with Python © Copyright 2020 Jason Brownlee. All Rights Reserved. Edition: v1.10

Jason Brownlee, PhD, Machine Learning Mastery

https://machinelearningmastery.com/develop-arch-and-garch-models-for-time-series-forecasting-in-python/

Thank you Jason for the countless hours and no doubt headaches and eye strain. You taught me that machine learning can be fun!

ARCH and GARCH Models in Python

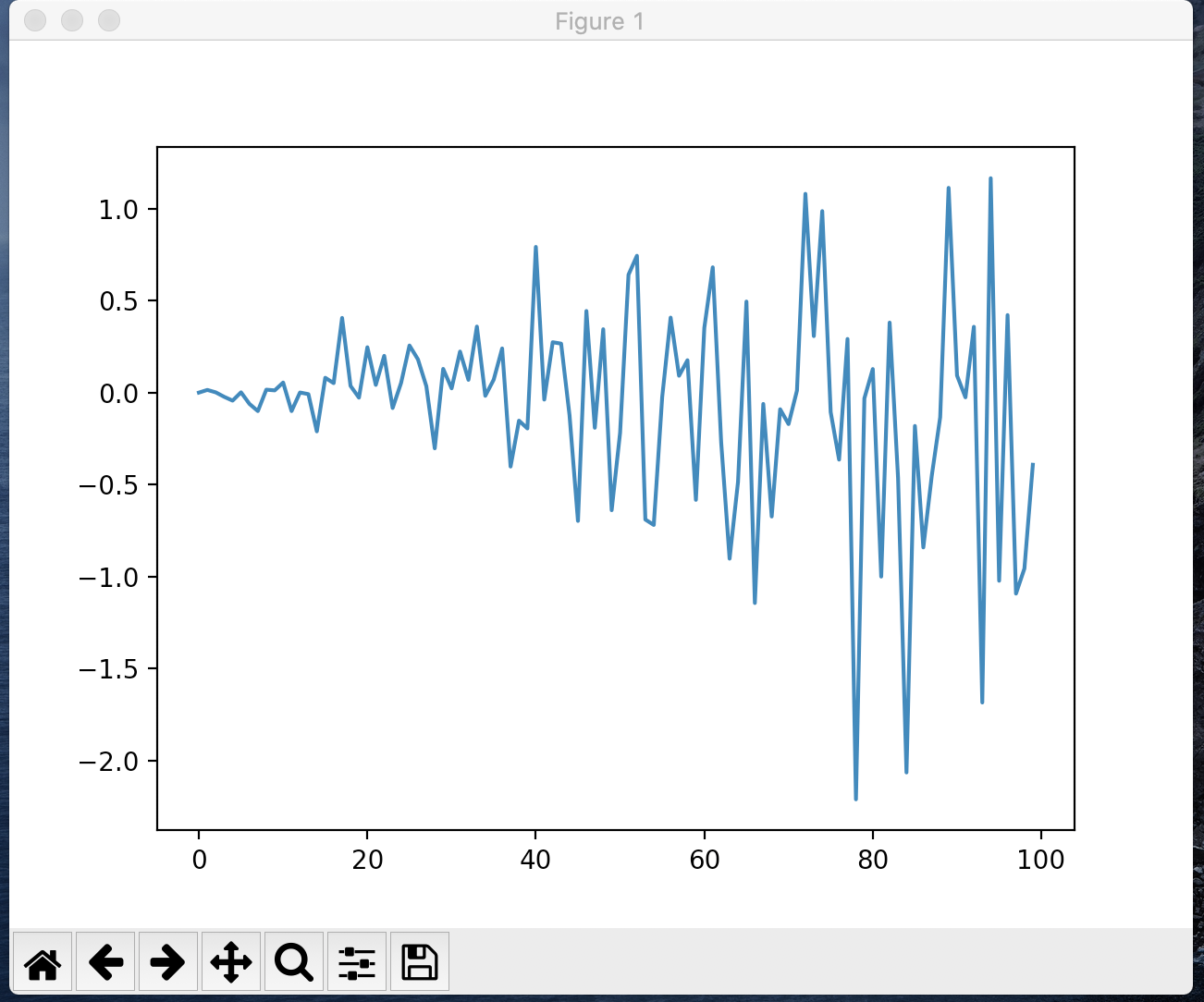

# create a simple white noise with increasing variance

from random import gauss

from random import seed

from matplotlib import pyplot

# seed pseudorandom number generator

seed(1)

# create dataset

data = [gauss(0, i*0.01) for i in range(0,100)]

# plot

pyplot.plot(data)

pyplot.show()

![enter image description here]()

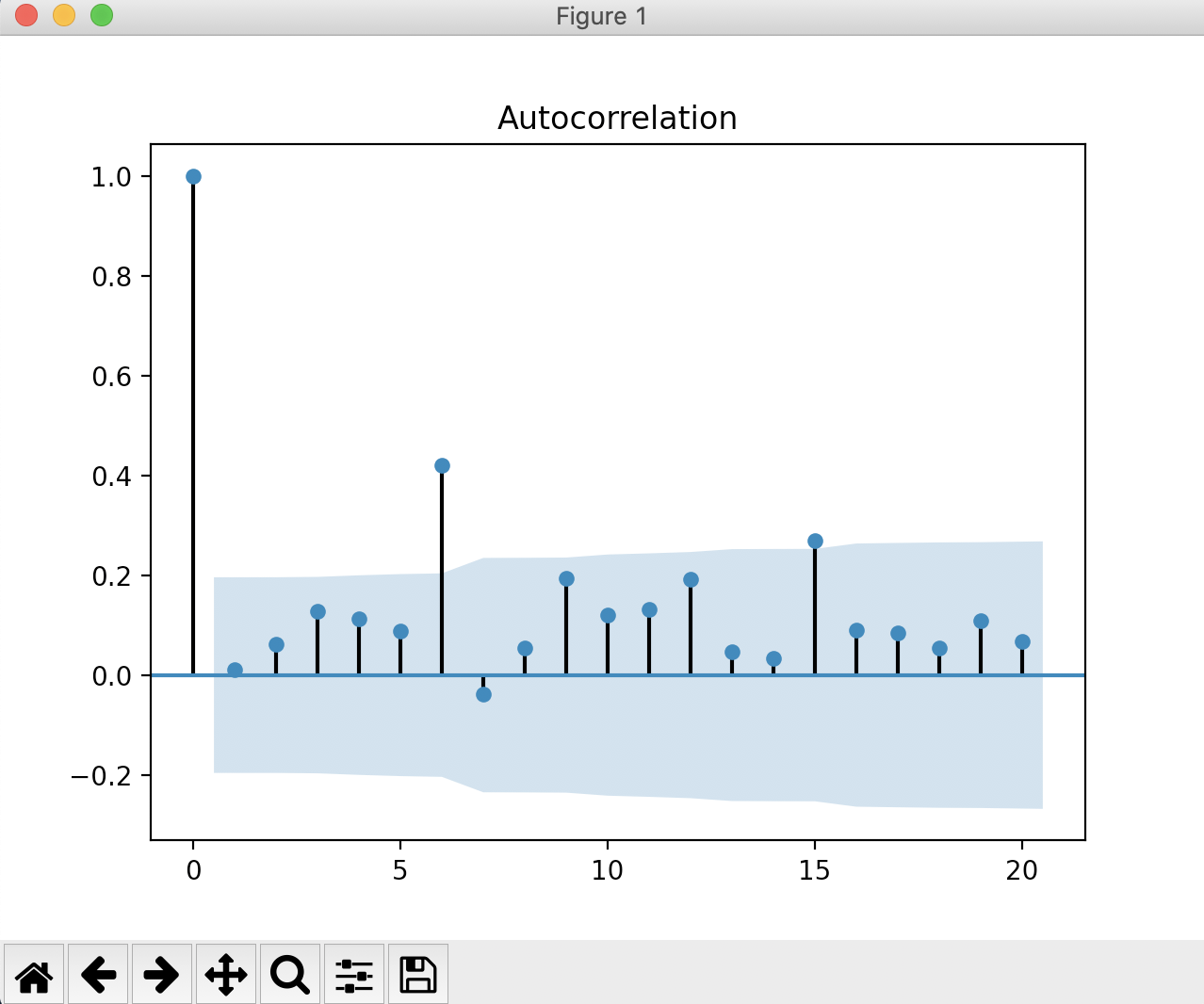

# create dataset

data = [gauss(0, i*0.01) for i in range(1,100+1)]

# check correlations of squared observations

from random import gauss

from random import seed

from matplotlib import pyplot

from statsmodels.graphics.tsaplots import plot_acf

# seed pseudorandom number generator

seed(1)

# create dataset

data = [gauss(0, i*0.01) for i in range(0,100)]

# square the dataset

squared_data = [x**2 for x in data]

# create acf plot

plot_acf(np.array(squared_data))

pyplot.show()

![enter image description here]()

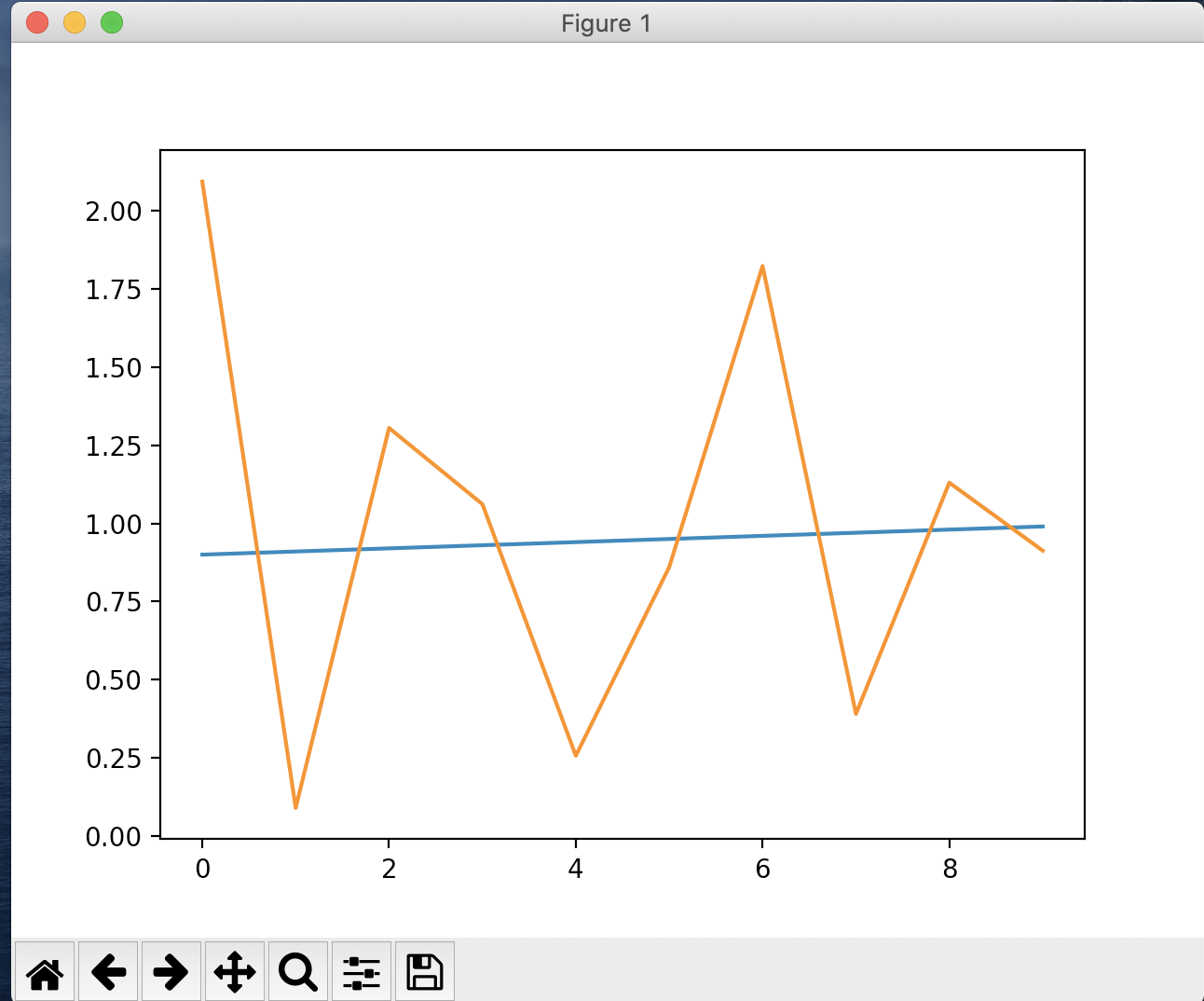

# split into train/test

n_test = 10

train, test = data[:-n_test], data[-n_test:]

# example of ARCH model

from random import gauss

from random import seed

from matplotlib import pyplot

from arch import arch_model

# seed pseudorandom number generator

seed(1)

# create dataset

data = [gauss(0, i*0.01) for i in range(0,100)]

# split into train/test

n_test = 10

train, test = data[:-n_test], data[-n_test:]

# define model

model = arch_model(train, mean='Zero', vol='ARCH', p=15)

# fit model

model_fit = model.fit()

# forecast the test set

yhat = model_fit.forecast(horizon=n_test)

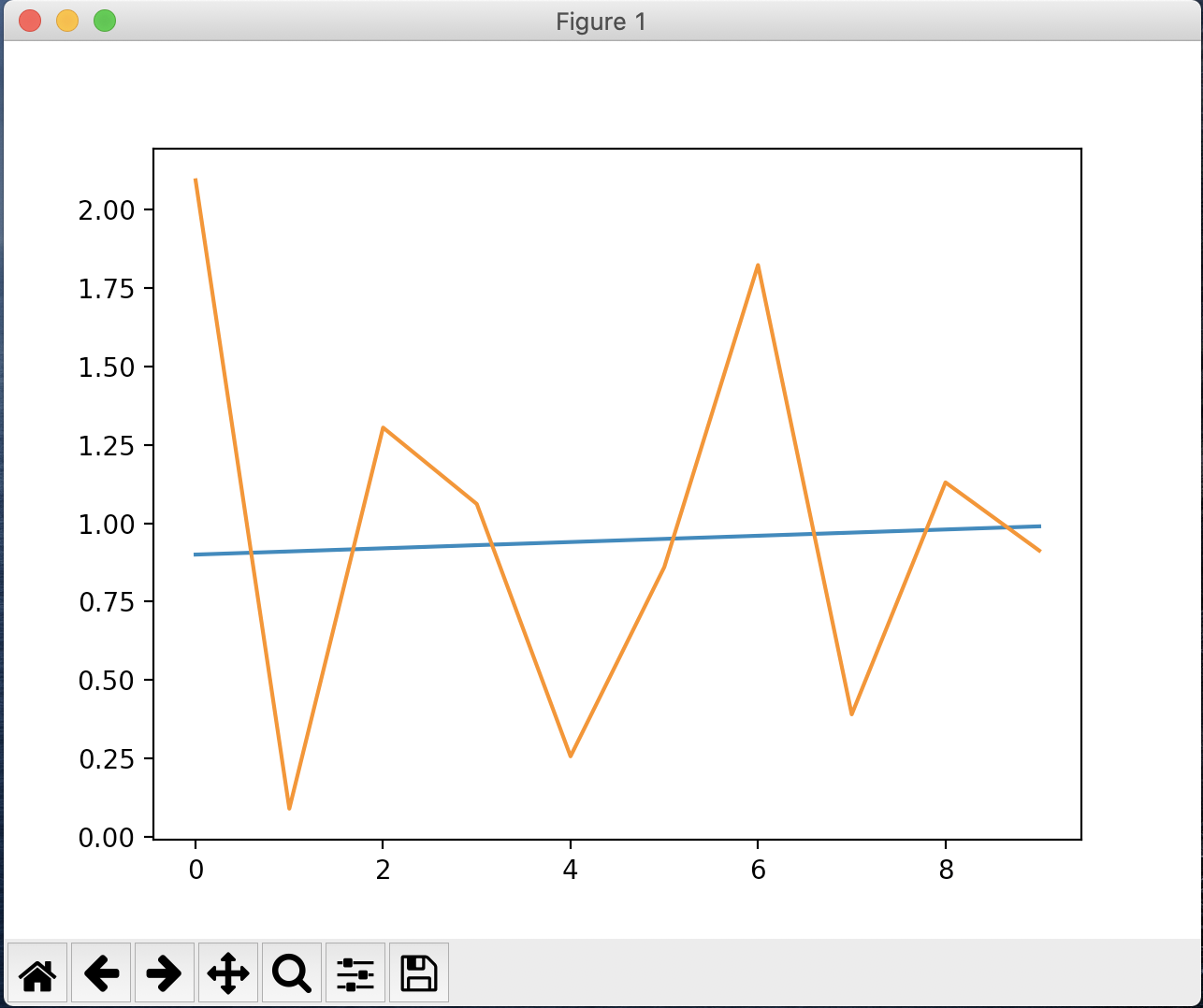

# plot the actual variance

var = [i*0.01 for i in range(0,100)]

pyplot.plot(var[-n_test:])

# plot forecast variance

pyplot.plot(yhat.variance.values[-1, :])

pyplot.show()

![enter image description here]()

![enter image description here]()

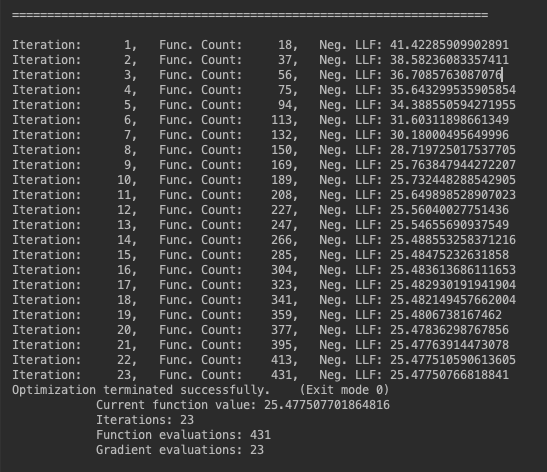

# example of ARCH model

# seed pseudorandom number generator

seed(1)

# create dataset

data = [gauss(0, i*0.01) for i in range(0,100)]

# split into train/test

n_test = 10

train, test = data[:-n_test], data[-n_test:]

# define model

model = arch_model(train, mean='Zero', vol='GARCH', p=15, q=15)

# fit model

model_fit = model.fit()

# forecast the test set

yhat = model_fit.forecast(horizon=n_test)

# plot the actual variance

var = [i*0.01 for i in range(0,100)]

pyplot.plot(var[-n_test:])

# plot forecast variance

pyplot.plot(yhat.variance.values[-1, :])

pyplot.show()

# define model

model = arch_model(train, mean='Zero', vol='GARCH', p=15, q=15)

![enter image description here]()

and see results are extremely similar, however with a little more than twice as many iterations...

![enter image description here]()

Citing reference Book:

Introduction to Time Series Forecasting with Python

© Copyright 2020 Jason Brownlee. All Rights Reserved. Edition: v1.10

Jason Brownlee, PhD, Machine Learning Mastery

https://machinelearningmastery.com/develop-arch-and-garch-models-for-time-series-forecasting-in-python/