Edit!

For anyone wondering this same thing, I figured it out. There is nothing wrong with the implementations below. Its just the fact that EMA requires more than 21 data points to count a 20 data point exponential moving average. The reason for this is that the earlier data points effect the datapoints you are trying to calculate. In simple terms you i tested and you need about 40-50 datapoints to get the same 20 day EMA as with 100+ datapoints.

I'm trying to calculate the EMA (Exponential moving average) of a stock, but there is something wrong with my calculations. I have exported the last 22+ days of stock data for AAPL, and when I try to calculate the EMA for this there is something wrong every time.

Here is the data for my example: https://pastebin.com/raw/2MsgCeQx

Here are the solutions that I have tried to calculate the 20 day EMA.

#Imported the data as "data".

#With Ta-lib

data["EMA20Talib"] = talib.EMA(data.uClose, timeperiod = 20)

#And with pandas

data["EMA20Pandas"] = data["uClose"].ewm(span=20, adjust = False).mean()

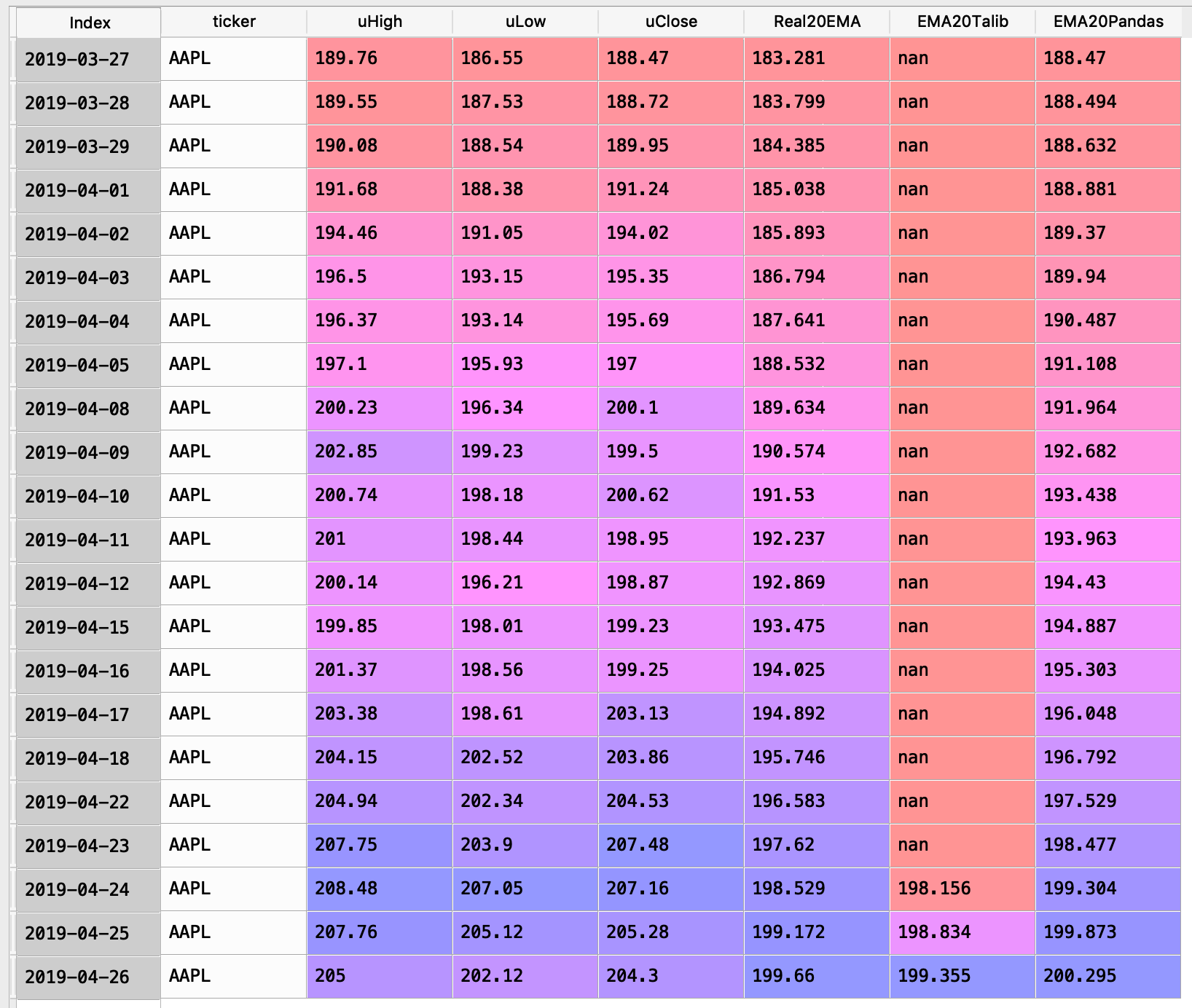

I here is an image of the data and the results. https://i.sstatic.net/B7IRi.png

{kind=link}

As you can see the Real20EMA does not match the TA-lib or the pandas 20EMA. What am I doing wrong?

The uClose is the column Im calulating the EMA on, the "Real20EMA" is taken from tradingview (cross referenced with marketwatch to make sure its the correct one).

I noticed that the there was a similar problem on here earlier with the same problem: Pandas' EMA not matching the stock's EMA?. The problem was solved there when you sorted the index, and I have made sure that I have it correctly sorted, but alas I still get the same problem.

I want to get the same numbers as the other finance sites using some tool. Weirdly enough even those two method I tried does not even return the same result.