I want to get a confidence interval of the result of a linear regression. I'm working with the boston house price dataset.

I've found this question: How to calculate the 99% confidence interval for the slope in a linear regression model in python? However, this doesn't quite answer my question.

Here is my code:

import numpy as np

import matplotlib.pyplot as plt

from math import pi

import pandas as pd

import seaborn as sns

from sklearn.datasets import load_boston

from sklearn.model_selection import train_test_split

from sklearn.linear_model import LinearRegression

from sklearn.metrics import mean_squared_error, r2_score

# import the data

boston_dataset = load_boston()

boston = pd.DataFrame(boston_dataset.data, columns=boston_dataset.feature_names)

boston['MEDV'] = boston_dataset.target

X = pd.DataFrame(np.c_[boston['LSTAT'], boston['RM']], columns=['LSTAT', 'RM'])

Y = boston['MEDV']

# splits the training and test data set in 80% : 20%

# assign random_state to any value.This ensures consistency.

X_train, X_test, Y_train, Y_test = train_test_split(X, Y, test_size=0.2, random_state=5)

lin_model = LinearRegression()

lin_model.fit(X_train, Y_train)

# model evaluation for training set

y_train_predict = lin_model.predict(X_train)

rmse = (np.sqrt(mean_squared_error(Y_train, y_train_predict)))

r2 = r2_score(Y_train, y_train_predict)

# model evaluation for testing set

y_test_predict = lin_model.predict(X_test)

# root mean square error of the model

rmse = (np.sqrt(mean_squared_error(Y_test, y_test_predict)))

# r-squared score of the model

r2 = r2_score(Y_test, y_test_predict)

plt.scatter(Y_test, y_test_predict)

plt.show()

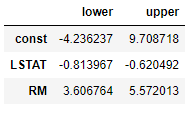

How can I get, for instance, the 95% or 99% confidence interval from this? Is there some sort of in-built function or piece of code?