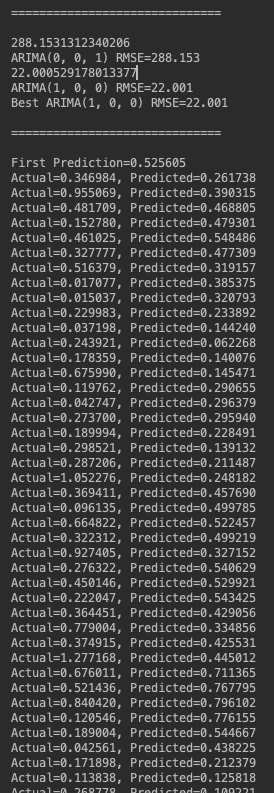

Background: I'm developing a program using statsmodels that fits 27 arima models (p,d,q=0,1,2) to over 100 variables and chooses the model with the lowest aic and statistically significant t-statistics for the AR/MA coefficients and statistically significant p-values for the dickey fuller test...

For one particular variable and one particular set of parameters, I get

LinAlgError: SVD did not converge

for replication, the variable and the code that fails are below

rollrate =[0.3469842191781748,

0.9550689157572028,

0.48170862494888256,

0.15277985674197356,

0.46102487817508747,

0.32777706854320243,

0.5163787896482797,

0.01707716528127215,

0.015036662424309755,

0.2299825242910243,

0.03719773802216722,

0.24392098372995807,

0.1783587055969874,

0.6759904243574179,

0.1197617555878022,

0.04274682226635633,

0.27369984820298465,

0.18999355015483932,

0.2985208240580264,

0.2872064881442138,

1.0522764728046277,

0.3694114556631419,

0.09613536093441034,

0.6648215681632191,

0.3223120091564835,

0.9274048223872483,

0.2763221143255601,

0.4501460109958479,

0.2220472247972312,

0.3644512582291407,

0.7790042237519584,

0.3749145302678043,

1.2771681290160286,

0.6760112486224217,

0.5214358465170098,

0.84041997296269,

0.12054593136059581,

0.18900376737686622,

0.042561102427304424,

0.17189805124670604,

0.11383752243305952,

0.2687780002387387,

0.717538770963329,

0.26636160206108384,

0.04221743047344771,

0.3259506533106764,

0.20146525340606328,

0.4059344185647537,

0.07503287726465639,

0.3011594076817088,

0.1433563136989911,

0.14803562944375281,

0.23096999679467808,

0.31133672787599703,

0.2313639154827471,

0.30343086620083537,

0.4608439884577555,

0.19149827372467804,

0.2506814947310181,

1.008458195025946,

0.3776434264127751,

0.344728062930179,

0.2110402015365776,

0.26582041849423843,

1.1019000121595244,

0.0,

0.023068095385979804,

0.014256779894199491,

0.3209225608633755,

0.00294468492742426,

0.0,

0.3346732726544143,

0.38256681208088283,

0.4916019617068597,

0.06922156984602362,

0.34458053250016984,

0.0,

0.09615667784109984,

1.8271531669931351,

0,

0,

0.0,

0,

0.0,

0.03205594450156685,

0.0,

0.0,

0.0,

0,

0.0,

0,

0.0,

0,

0,

1.0,

0]

p=2

q=2

d=0

fit = statsmodels.api.tsa.ARIMA(rollRate, (p,d,q)).fit(transparams=False)

I understand that the particular parameters p=2,d=2,q=0 may be a terrible ARIMA model for this particular variable and that the variable itself may not be a suitable candidate for an ARIMA model due to the many zeroes or unstationary qualities, but I need a way to possibly bypass this error or fix the issue in order to keep the program iterating through parameters. Thanks

try-exceptblock? This way you accept that for some parameter combinations your selected model cannot be fitted. – Chambermaidtry: fit = statsmodels.api.tsa.ARIMA(rollRate, (p,d,q)).fit(transparams=False) except (ValueError, LinAlgError): passbut i get aNameError: name 'LinAlgError' is not defined– HutchingsLinAlgErrorto your namespace:from numpy.linalg import LinAlgError– Chambermaid_safe_arma_fit. It also handles the cases of non-convergence due to bad starting parameters. All pretty naive though. github.com/statsmodels/statsmodels/blob/master/statsmodels/tsa/… – Celindaceline_safe_arma_fitwork ? – Taegu