Without any additional packages:

true_Y = c(1,1,1,1,2,1,2,1,2,2)

probs = c(1,0.999,0.999,0.973,0.568,0.421,0.382,0.377,0.146,0.11)

getROC_AUC = function(probs, true_Y){

probsSort = sort(probs, decreasing = TRUE, index.return = TRUE)

val = unlist(probsSort$x)

idx = unlist(probsSort$ix)

roc_y = true_Y[idx];

stack_x = cumsum(roc_y == 2)/sum(roc_y == 2)

stack_y = cumsum(roc_y == 1)/sum(roc_y == 1)

auc = sum((stack_x[2:length(roc_y)]-stack_x[1:length(roc_y)-1])*stack_y[2:length(roc_y)])

return(list(stack_x=stack_x, stack_y=stack_y, auc=auc))

}

aList = getROC_AUC(probs, true_Y)

stack_x = unlist(aList$stack_x)

stack_y = unlist(aList$stack_y)

auc = unlist(aList$auc)

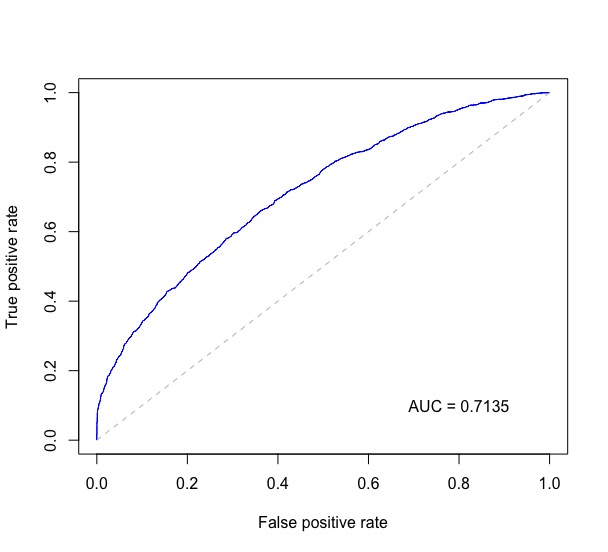

plot(stack_x, stack_y, type = "l", col = "blue", xlab = "False Positive Rate", ylab = "True Positive Rate", main = "ROC")

axis(1, seq(0.0,1.0,0.1))

axis(2, seq(0.0,1.0,0.1))

abline(h=seq(0.0,1.0,0.1), v=seq(0.0,1.0,0.1), col="gray", lty=3)

legend(0.7, 0.3, sprintf("%3.3f",auc), lty=c(1,1), lwd=c(2.5,2.5), col="blue", title = "AUC")

![enter image description here]()