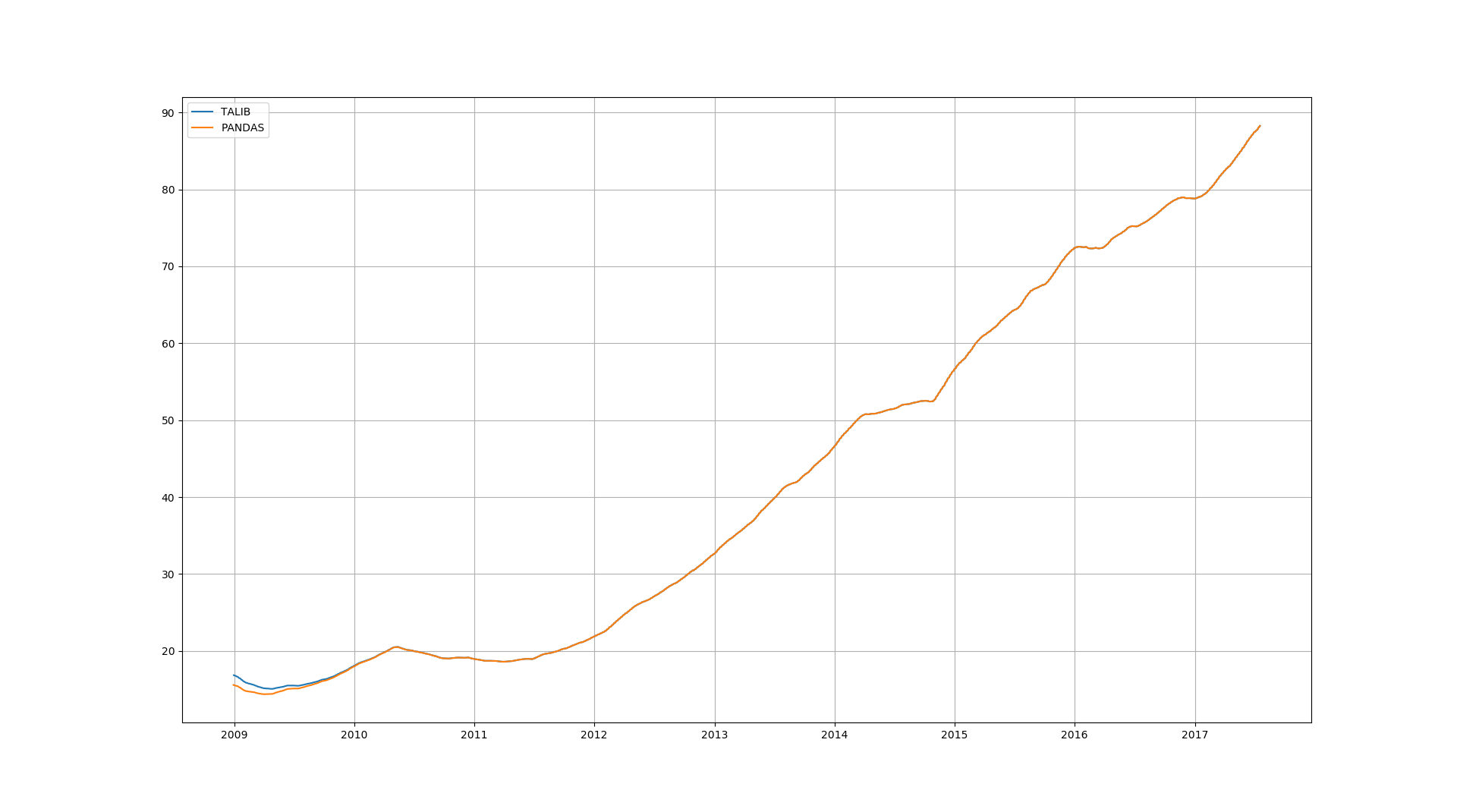

I'm currently writng a code involving some financial calculation. More in particular some exponential moving average. To do the job I have tried Pandas and Talib:

talib_ex=pd.Series(talib.EMA(self.PriceAdjusted.values,timeperiod=200),self.PriceAdjusted.index)

pandas_ex=self.PriceAdjusted.ewm(span=200,adjust=True,min_periods=200-1).mean()

They both work fine, but they provide different results at the begining of the array:

So there is some parameter to be change into pandas's EWMA or it is a bug and I should worry?

Thanks in advance

Luca