I would like to make a "ggplot version" of the basic functionality of charts.PerformanceSummary that is available in the PerformanceAnalytics package, as I think that ggplot is generally prettier and theoretically more powerful in term of editing the image. I've got reasonably close but have a few issues that I would like a bit of help on. Namely:

- reducing the amount of space that the legend takes up, it gets horrendous/ugly when having more than 10 lines on it...(just the line colour and name is sufficient)

- Increasing the size of the Daily_Returns facet to match that of charts.PerformanceSummary in

PerformanceAnalytics - Have an option that specifies which asset to show in the daily return series in the Daily_Returns facet, rather than always using the first column, which is than what happens in

charts.PerformanceSummary

If there are better ways to do this potentially using gridExtra rather than facets...I'm not adverse to people showing me how that would look better...

The issue here is aesthetics, and potential easy of manipulation I guess, as PerformanceAnalytics already has a good working example, I just want to make it prettier/more professional...

In addition to this for bonus points, I would like to be able to show some performance stats associated with it somewhere on or below or to the side of the graph for each asset...not too sure where would be best to show or display this information.

Furthermore I am not adverse to people suggesting parts that clean up my code if they have suggestions for this.

Here is my reproducible example...

First generate return data:

require(xts)

X.stock.rtns <- xts(rnorm(1000,0.00001,0.0003), Sys.Date()-(1000:1))

Y.stock.rtns <- xts(rnorm(1000,0.00003,0.0004), Sys.Date()-(1000:1))

Z.stock.rtns <- xts(rnorm(1000,0.00005,0.0005), Sys.Date()-(1000:1))

rtn.obj <- merge(X.stock.rtns , Y.stock.rtns, Z.stock.rtns)

colnames(rtn.obj) <- c("x.stock.rtns","y.stock.rtns","z.stock.rtns")

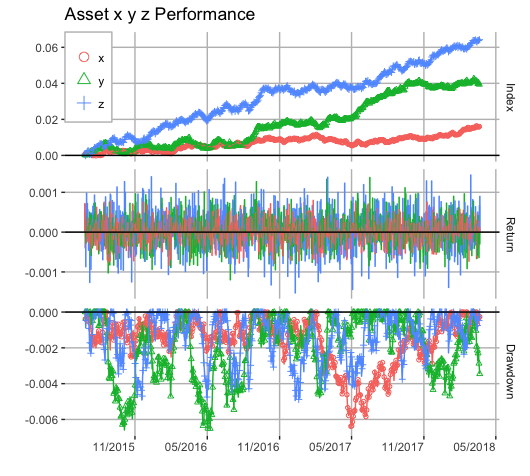

I would like to replicate the image from the result of:

require(PerformanceAnalytics)

charts.PerformanceSummary(rtn.obj, geometric=TRUE)

This is my attempt so far...

gg.charts.PerformanceSummary <- function(rtn.obj, geometric=TRUE, main="",plot=TRUE){

# load libraries

suppressPackageStartupMessages(require(ggplot2))

suppressPackageStartupMessages(require(scales))

suppressPackageStartupMessages(require(reshape))

suppressPackageStartupMessages(require(PerformanceAnalytics))

# create function to clean returns if having NAs in data

clean.rtn.xts <- function(univ.rtn.xts.obj,na.replace=0){

univ.rtn.xts.obj[is.na(univ.rtn.xts.obj)]<- na.replace

univ.rtn.xts.obj

}

# Create cumulative return function

cum.rtn <- function(clean.xts.obj, g=TRUE){

x <- clean.xts.obj

if(g==TRUE){y <- cumprod(x+1)-1} else {y <- cumsum(x)}

y

}

# Create function to calculate drawdowns

dd.xts <- function(clean.xts.obj, g=TRUE){

x <- clean.xts.obj

if(g==TRUE){y <- Drawdowns(x)} else {y <- Drawdowns(x,geometric=FALSE)}

y

}

# create a function to create a dataframe to be usable in ggplot to replicate charts.PerformanceSummary

cps.df <- function(xts.obj,geometric){

x <- clean.rtn.xts(xts.obj)

series.name <- colnames(xts.obj)[1]

tmp <- cum.rtn(x,geometric)

tmp$rtn <- x

tmp$dd <- dd.xts(x,geometric)

colnames(tmp) <- c("Cumulative_Return","Daily_Return","Drawdown")

tmp.df <- as.data.frame(coredata(tmp))

tmp.df$Date <- as.POSIXct(index(tmp))

tmp.df.long <- melt(tmp.df,id.var="Date")

tmp.df.long$asset <- rep(series.name,nrow(tmp.df.long))

tmp.df.long

}

# A conditional statement altering the plot according to the number of assets

if(ncol(rtn.obj)==1){

# using the cps.df function

df <- cps.df(rtn.obj,geometric)

# adding in a title string if need be

if(main==""){

title.string <- paste0(df$asset[1]," Performance")

} else {

title.string <- main

}

# generating the ggplot output with all the added extras....

gg.xts <- ggplot(df, aes_string(x="Date",y="value",group="variable"))+

facet_grid(variable ~ ., scales="free", space="free")+

geom_line(data=subset(df,variable=="Cumulative_Return"))+

geom_bar(data=subset(df,variable=="Daily_Return"),stat="identity")+

geom_line(data=subset(df,variable=="Drawdown"))+

ylab("")+

geom_abline(intercept=0,slope=0,alpha=0.3)+

ggtitle(title.string)+

theme(axis.text.x = element_text(angle = 45, hjust = 1))+

scale_x_datetime(breaks = date_breaks("6 months"), labels = date_format("%d/%m/%Y"))

} else {

# a few extra bits to deal with the added rtn columns

no.of.assets <- ncol(rtn.obj)

asset.names <- colnames(rtn.obj)

df <- do.call(rbind,lapply(1:no.of.assets, function(x){cps.df(rtn.obj[,x],geometric)}))

df$asset <- ordered(df$asset, levels=asset.names)

if(main==""){

title.string <- paste0(df$asset[1]," Performance")

} else {

title.string <- main

}

if(no.of.assets>5){legend.rows <- 5} else {legend.rows <- no.of.assets}

gg.xts <- ggplot(df, aes_string(x="Date", y="value",group="asset"))+

facet_grid(variable~.,scales="free",space="free")+

geom_line(data=subset(df,variable=="Cumulative_Return"),aes(colour=factor(asset)))+

geom_bar(data=subset(df,variable=="Daily_Return"),stat="identity",aes(fill=factor(asset),colour=factor(asset)),position="dodge")+

geom_line(data=subset(df,variable=="Drawdown"),aes(colour=factor(asset)))+

ylab("")+

geom_abline(intercept=0,slope=0,alpha=0.3)+

ggtitle(title.string)+

theme(legend.title=element_blank(), legend.position=c(0,1), legend.justification=c(0,1),

axis.text.x = element_text(angle = 45, hjust = 1))+

guides(col=guide_legend(nrow=legend.rows))+

scale_x_datetime(breaks = date_breaks("6 months"), labels = date_format("%d/%m/%Y"))

}

assign("gg.xts", gg.xts,envir=.GlobalEnv)

if(plot==TRUE){

plot(gg.xts)

} else {}

}

# seeing the ggplot equivalent....

gg.charts.PerformanceSummary(rtn.obj, geometric=TRUE)