I'll experiment with the following dataframe.

Setup

import pandas as pd

import numpy as np

from string import uppercase

def generic_portfolio_df(start, end, freq, num_port, num_sec, seed=314):

np.random.seed(seed)

portfolios = pd.Index(['Portfolio {}'.format(i) for i in uppercase[:num_port]],

name='Portfolio')

securities = ['s{:02d}'.format(i) for i in range(num_sec)]

dates = pd.date_range(start, end, freq=freq)

return pd.DataFrame(np.random.rand(len(dates) * num_sec, num_port),

index=pd.MultiIndex.from_product([dates, securities],

names=['Date', 'Id']),

columns=portfolios

).groupby(level=0).apply(lambda x: x / x.sum())

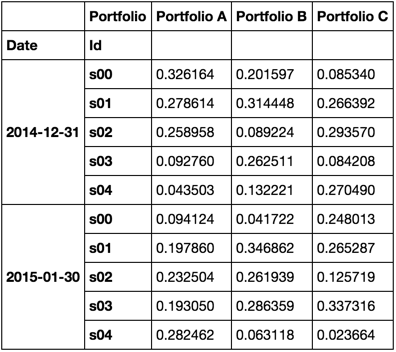

df = generic_portfolio_df('2014-12-31', '2015-05-30', 'BM', 3, 5)

df.head(10)

![enter image description here]()

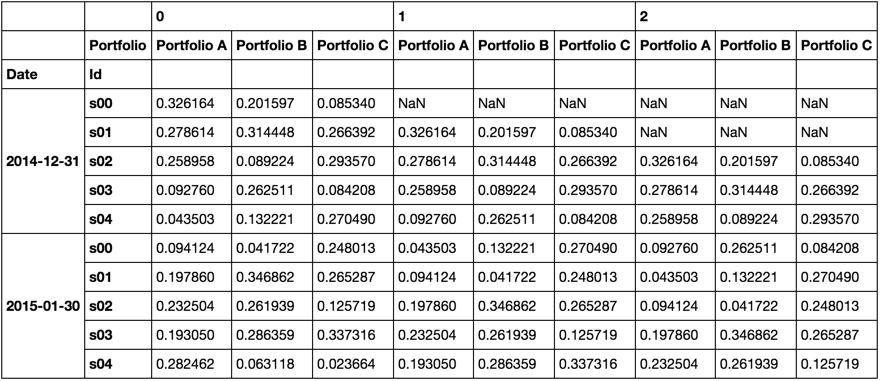

I'll now introduce a function to roll a number of rows and concatenate into a single dataframe where I'll add a top level to the column index that indicates the location in the roll.

Solution Step-1

def rolled(df, n):

k = range(df.columns.nlevels)

_k = [i - len(k) for i in k]

myroll = pd.concat([df.shift(i).stack(level=k) for i in range(n)],

axis=1, keys=range(n)).unstack(level=_k)

return [(i, row.unstack(0)) for i, row in myroll.iterrows()]

Though its hidden in the function, myroll would look like this

![enter image description here]()

Now we can use it just like an iterator.

Solution Step-2

for i, roll in rolled(df.head(5), 3):

print roll

print

0 1 2

Portfolio

Portfolio A 0.326164 NaN NaN

Portfolio B 0.201597 NaN NaN

Portfolio C 0.085340 NaN NaN

0 1 2

Portfolio

Portfolio A 0.278614 0.326164 NaN

Portfolio B 0.314448 0.201597 NaN

Portfolio C 0.266392 0.085340 NaN

0 1 2

Portfolio

Portfolio A 0.258958 0.278614 0.326164

Portfolio B 0.089224 0.314448 0.201597

Portfolio C 0.293570 0.266392 0.085340

0 1 2

Portfolio

Portfolio A 0.092760 0.258958 0.278614

Portfolio B 0.262511 0.089224 0.314448

Portfolio C 0.084208 0.293570 0.266392

0 1 2

Portfolio

Portfolio A 0.043503 0.092760 0.258958

Portfolio B 0.132221 0.262511 0.089224

Portfolio C 0.270490 0.084208 0.293570